Apple Stock Hits All-Time High +51%: Genius Strategy or Dangerous Gamble on AI?

July 14, 2026

The headline that has Wall Street divided

Apple just hit an all-time high. Up 51% in the past 12 months, AAPL has outperformed nearly every mega-cap in the S&P 500 — a remarkable achievement for a company that, by most metrics, is spending far less on artificial intelligence than every one of its primary competitors.

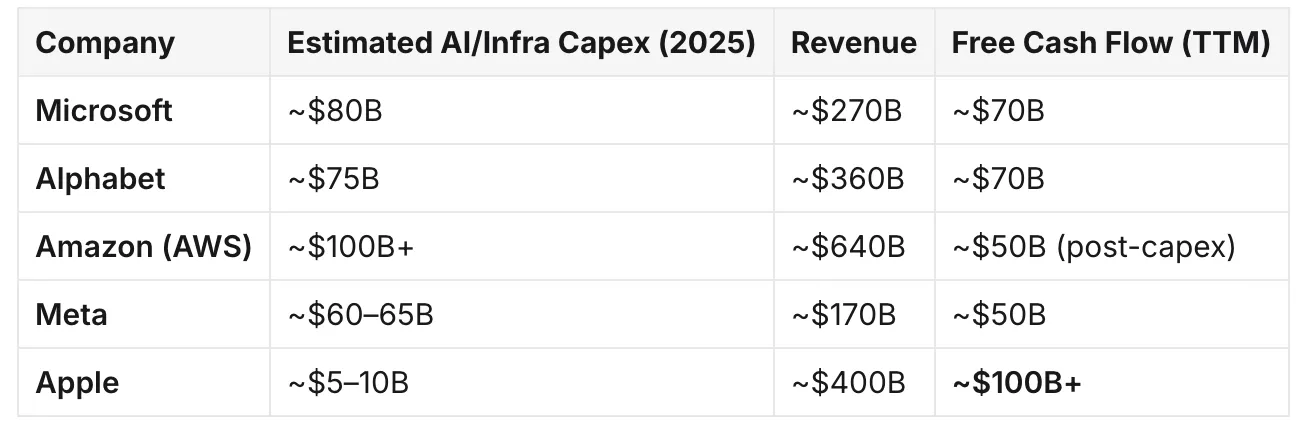

Microsoft is pouring $80+ billion into AI infrastructure this fiscal year. Meta has committed $60–65 billion in capex for 2025. Alphabet is spending $75 billion. Amazon's cloud and AI buildout is running at $100+ billion annually. Apple? Estimates place Apple's AI-specific capital expenditure at $5–10 billion — a fraction of what any of its Big Tech peers are deploying.

And yet Apple's stock is at an all-time high.

The question every serious investor needs to answer right now: Is Apple making the smartest move in tech — or quietly setting itself up for the most painful strategic miss of the decade?

The Numbers: Apple vs Big Tech AI Spending

Apple's free cash flow is the highest in absolute terms among all Big Tech. Its AI underspend is not an accident — it is a deliberate capital allocation thesis. The question is whether that thesis holds as AI competes for consumer attention, enterprise contracts, and platform dominance.

Why Apple Is Spending Less — And Why It Might Be Right

1. Apple's AI is Already Embedded in Its Products

Apple doesn't need a cloud-scale AI buildout the way Microsoft or Amazon does, because Apple's AI strategy is fundamentally on-device first. The Apple Neural Engine — embedded in every M-series chip and A-series mobile chip — processes AI tasks locally without routing to expensive cloud infrastructure.

This architecture means Apple can offer AI features like predictive text, photo processing, Face ID, and increasingly Apple Intelligence without paying for massive server farms per query. The marginal cost of AI at Apple is far lower per user than at Microsoft (Azure AI) or Alphabet (Gemini cloud).

2. Apple Intelligence Is Playing the Long Game — Quietly

Apple Intelligence, announced at WWDC 2024 and rolling out through 2025, is not a ChatGPT killer. It is a deeply integrated suite of AI features baked into iOS, macOS, and iPadOS. Features include:

- Writing tools across every native app

- Priority notifications and intelligent summarization

- Photo search and generation (Image Playground)

- Siri with contextual, multi-step reasoning (powered by both on-device models and an OpenAI partnership for complex queries)

- Personal context awareness across Calendar, Mail, Messages

The key insight: Apple's AI is not a product. It is an upgrade cycle trigger. Every iPhone 15 and below cannot run Apple Intelligence. Every iPhone 16 can. This is the largest hardware upgrade catalyst Apple has engineered since Face ID in 2017.

3. The OpenAI Partnership Changes the Capex Math

Apple made a strategically shrewd move by partnering with OpenAI for ChatGPT integration directly into Siri — without building a frontier model from scratch. Apple essentially outsourced the most expensive part of the AI stack (training trillion-parameter models) while retaining the most valuable part: the interface layer and the 2.2 billion active devices.

For Apple, the $5–10B in AI spend does not tell the full story. It is leveraging OpenAI's $100B+ in investment at zero training cost while capturing the user-facing AI experience.

4. Free Cash Flow Fortress — The Buyback Machine

Apple's ~$100B in annual free cash flow funds the most aggressive share buyback program in corporate history. Since 2012, Apple has returned over $700 billion to shareholders via buybacks. This mechanically reduces share count, increasing EPS even in years of flat revenue growth.

With minimal AI capex, Apple preserves more FCF for buybacks. This is partly why the stock has hit ATH even as revenue growth has been modest: fewer shares outstanding means higher earnings per share, supporting a higher stock price.

The Bear Case: Why Apple Could Deeply Regret This

This is where the analysis gets uncomfortable — because the bear case is not trivial.

1. AI Could Disrupt Apple's Most Valuable Asset: The Ecosystem Lock-In

Apple's moat is the ecosystem. Users stay on iPhone because of iMessage, AirDrop, AirPods pairing, and the seamless hardware-software integration. But if AI assistants become the primary interface through which users interact with their digital lives — and that assistant is Microsoft Copilot, Google Gemini, or a standalone AI agent — the question becomes: does it matter what hardware you use?

If the AI layer becomes device-agnostic, Apple's ecosystem advantage erodes. A user who primarily interacts with the world through a powerful cloud-based AI agent has less reason to stay locked into Apple's ecosystem.

2. Enterprise Is Being Rewired — Without Apple

Microsoft's Copilot is being embedded into every Office 365 seat, Teams meeting, Excel spreadsheet, and PowerPoint presentation used by corporate enterprises globally. Alphabet's Gemini is restructuring Google Workspace. The enterprise software layer — where Microsoft and Google earn enormous, recurring revenue — is being fundamentally rebuilt around AI.

Apple has virtually no enterprise software revenue. Its enterprise exposure is hardware (MacBooks, iPhones for business). If enterprises begin standardizing on AI-powered software ecosystems from Microsoft or Google, Apple's enterprise hardware sales could face structural headwinds Apple has no AI product to counter.

3. The Search Revenue Risk Is Existential

Apple earns an estimated $18–20 billion per year from Google for making Google the default search engine on iOS and Safari. This is pure high-margin revenue — no cost of goods, no infrastructure, just a licensing fee.

The DOJ antitrust ruling against Google's search monopoly directly threatens this deal. More critically: if AI search (Perplexity, ChatGPT Search, Google AI Mode) replaces traditional web search, the value of the Google-Apple search deal collapses. This is a single line item that represents roughly 15–20% of Apple's operating income — and it could disappear within 3–5 years.

4. Siri Is Still Years Behind — And Users Know It

Despite Apple Intelligence, Siri remains widely perceived as the weakest AI assistant among the major platforms. Google Assistant, ChatGPT, and even Samsung's Galaxy AI have outpaced Siri in practical capability. If Apple's device upgrade cycle story requires Apple Intelligence to be compelling — but Apple Intelligence is perceived as second-tier — the upgrade cycle may disappoint.

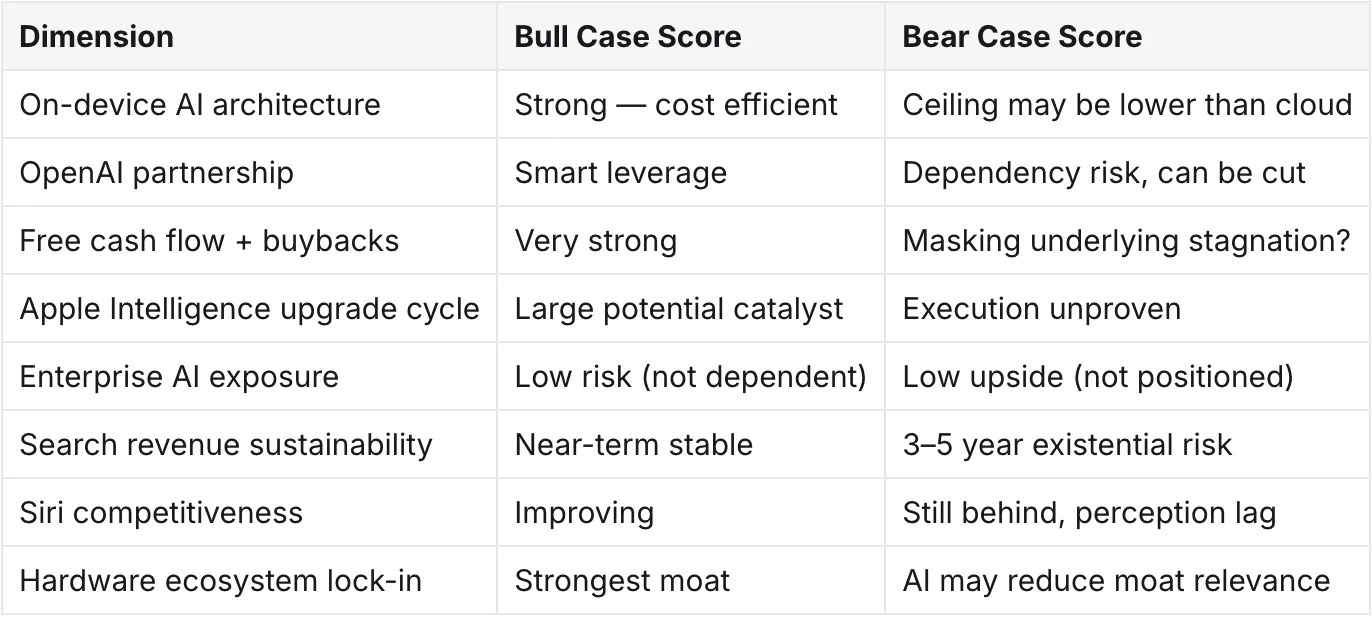

Bull vs Bear: The Scorecard

Net assessment: Apple's strategy is defensible for the next 12–24 months. The FCF flywheel, the upgrade cycle thesis, and the on-device AI architecture all support the current valuation. The bear case becomes dangerous in the 2027–2030 window — when Microsoft, Meta, and Alphabet's AI investments begin generating compounding returns that change enterprise and consumer software dynamics at scale.

What History Tells Us: The "Underspend and Catch Up" Playbook

Apple has been written off for underspending before:

- Cloud (2010–2015): Amazon and Google built massive cloud infrastructure. Apple built iCloud — a modest, user-facing product. Apple did not attempt to compete in enterprise cloud. Result: Apple lost the enterprise cloud market entirely. It didn't matter — because the iPhone drove $300B+ in revenue that dwarfed cloud.

- Search (never): Apple never built a search engine despite decades of Google default revenue. Critics said this would be Apple's downfall. It wasn't — Apple just collected the toll.

- Social (never): Ping, the failed music social network, was Apple's only attempt. Facebook, Instagram, TikTok dominate. Apple makes money from their App Store fees instead.

The pattern: Apple consistently lets competitors build categories, then either acquires what it needs, partners strategically, or builds a sufficiently good version for its installed base. The question is whether AI is categorically different — whether it is the infrastructure of the next computing era (like the internet was), not just another feature category.

If AI is truly the next platform shift, Apple's underinvestment today is more analogous to a telecom company in 1995 deciding not to invest in the internet because landline revenue was strong. That is the scenario that should concern Apple investors.

The Verdict: Right Bet for Now. Watch 2027.

Apple at ATH with +51% gains over 12 months reflects a market that believes the FCF fortress, the upgrade cycle, and the on-device AI strategy are sufficient for the near term. That belief is reasonable.

The stock is not pricing in the risk of the search revenue cliff, the enterprise AI irrelevance scenario, or the possibility that Siri falls permanently behind in the AI assistant race. Those are 2027–2030 risks — and markets are notoriously bad at pricing 3-year structural risks when short-term earnings are strong.

For investors today:

- The 12–24 month bull case is intact — FCF, buybacks, and upgrade cycle support the stock

- The 3–5 year risk-reward is more complicated than the ATH headline suggests

- Apple's AI bet is not reckless — it is a different risk profile than its peers, not necessarily a wrong one

- The $18–20B Google search deal is the single most important line item to watch

Apple is not making a dumb bet. It may be making a brilliant one. But the margin for error is narrowing as the AI race accelerates — and the companies now spending $60–100B per year on AI will begin to see returns that compound in ways that become very difficult to catch up to.

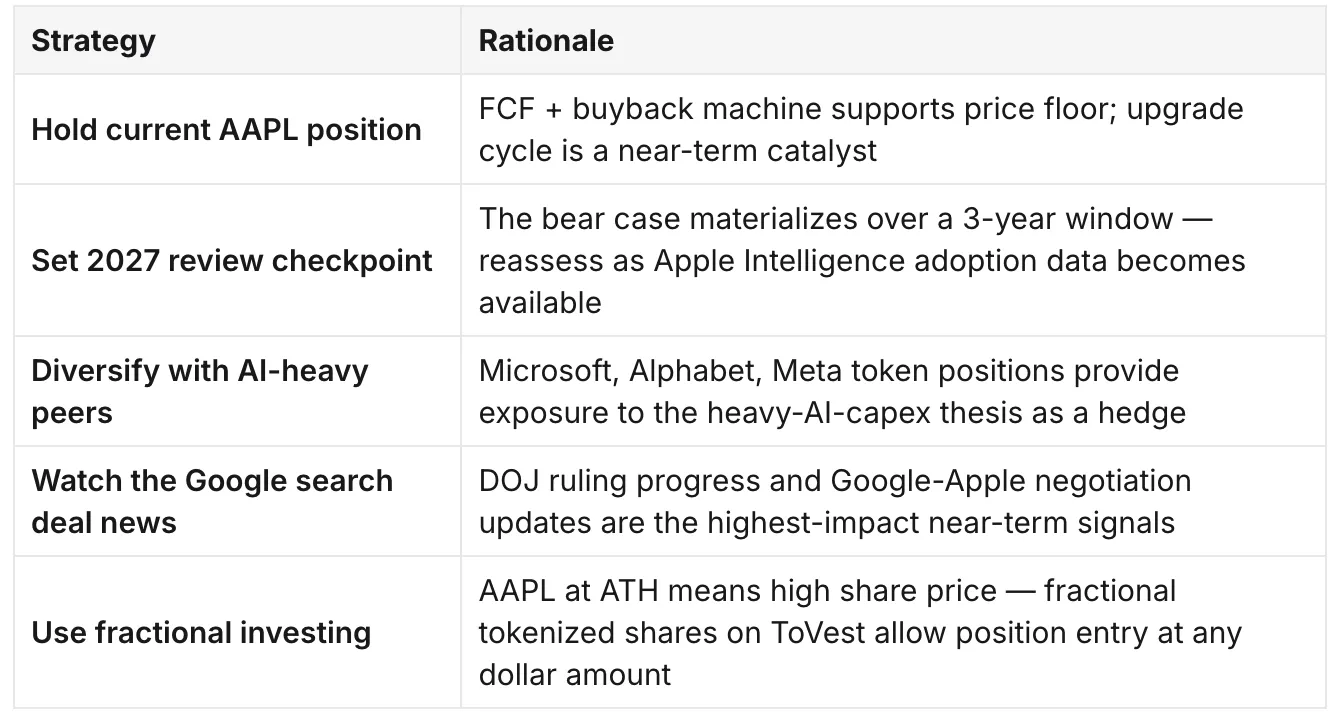

What This Means for ToVest Investors

Apple (AAPL) remains one of the most widely held tokenized equities on the ToVest platform. The ATH milestone and the strategic narrative above translate directly into practical investment considerations:

Frequently Asked Questions (FAQ)

Q: Why is Apple stock at all-time high if it's spending less on AI than competitors?

A: Apple's ATH is driven by three factors: massive free cash flow (~$100B/year) funding record share buybacks, the anticipated iPhone 16 upgrade cycle powered by Apple Intelligence, and investor confidence in Apple's on-device AI architecture as a capital-efficient alternative to cloud-heavy AI buildouts.

Q: Is Apple's low AI spending a risk?

A: In the 12–24 month window, the risk is manageable. The structural risk emerges in 2027–2030, when Microsoft's Copilot, Meta's AI, and Google's Gemini ecosystem investments begin compounding returns at enterprise and consumer scale that Apple may struggle to match.

Q: What is Apple's actual AI strategy?

A: Apple's AI strategy has three pillars: on-device processing via the Apple Neural Engine (privacy-preserving, low-cost); Apple Intelligence as an iOS/macOS upgrade cycle trigger; and a strategic OpenAI partnership for complex cloud-based queries — outsourcing frontier model costs while retaining the user interface layer across 2.2 billion devices.

Q: What is Apple's biggest financial risk right now?

A: The Google search revenue deal — estimated at $18–20 billion annually — is Apple's single largest financial risk. The DOJ antitrust ruling against Google and the structural shift toward AI search both threaten this revenue stream within a 3–5 year window.

Q: Can I invest in Apple stock without buying a full share?

A: Yes. ToVest offers tokenized Apple stock (AAPL) with fractional investment — you can buy as little as $1 worth of AAPL exposure, settled in USDT, available 24/7 without a traditional brokerage account.

Q: Is Apple a good investment at ATH?

A: The FCF thesis and buyback program provide a strong structural floor. At ATH, the near-term upside is more limited and downside risks are more asymmetric. A phased entry strategy — buying fractional positions over time rather than all at once — reduces timing risk in a stock trading at peak valuations.

Invest in tokenized Apple stock on ToVest — fractional, 24/7, settled in USDT. Start with any amount.